When people think about business valuation, they tend to focus on the most discussed elements: revenue, profit margins, and growth rates. And while those are important, they’re not actually where all of the controllable leverage lies.

In professional valuation work, the foundation is almost always the Discounted Cash Flow (DCF) method. In a DCF, we project a company’s future cash flows, then convert those projected future dollars into a present-day value. This allows us to estimate what the business is worth today.

There are, of course, other valuation approaches (multiple of ____, liquidation value, book value), but DCF is the most important because it is the foundation of many other methods. It attempts to answer the question, if I want to receive x% return, what $y should I be willing to pay for this business, based on what it will earn in the future?

None of that is surprising. What is surprising, and what most business owners never think about, is the most critical input of all:

The Discount Rate Itself

The discount rate determines how heavily future cash flows are “penalized” for time, risk, and uncertainty. The higher the perceived risk, the higher the discount rate. And the higher the discount rate, the lower the valuation.

Adjusting this one input to the valuation model can easily swing the value of a business by 30%, 50%, or even more.

An earnings multiple is just another way of looking at the discount rate. In admittedly over-simplified terms (expected growth is a factor in real life), if I'd need to earn a 20% return in order to buy your business, and the business produces $1m of profit per year, I'd have to pay $5m. 5x is the multiple of earnings, and 20% is the required rate of return.

They are two expressions of the same idea, and the multiple is the inverse of the rate (100% over 20% = 5x). The main complication comes from the fact that future earnings may or may not be much higher or lower than this year's, and the likelihood of (and time until) each of those years of profit have a lot to do with what a company is worth today.

Despite its real-world ubiquity, very few owners understand what the discount rate really represents, how it is determined, how it varies, and what it's made of. For example, how does one decide what expected return they would need in order to buy your business?

Here’s the good news:

You can break the discount rate into parts. And when you do, it becomes a powerful diagnostic tool that tells the story of your business’s strength, resilience, and risk. If you can alter the discount rate appropriately applied to your business, you can change what it's worth to others - and how valuable it is to you.

The Components of the Discount Rate

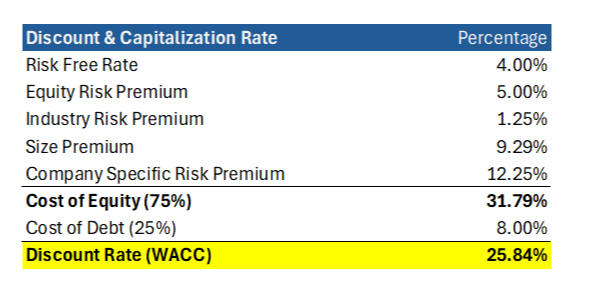

The total discount rate used in valuation is built from five primary building blocks:

- Risk-Free Rate

- Equity Risk Premium

- Industry Risk Premium

- Size Premium

- Company-Specific Risk Premium

Some of these factors are completely outside your control. Others are largely within your control. Understanding what you control is where the magic can happen.

Note: As you can see above, there's an element of this which is the total cost of capital, which weighs borrowing cost into the mix. The conversation in this blog post is deliberately simplified to exclude that component.

Part 1: What You Don’t Control

1. Risk-Free Rate

This is the baseline cost of money in the economy, often represented by U.S. Federal government bond yields. It reflects macroeconomic forces and government policy, not your business. Since it's by definition the "risk free" rate it reflects the time value of money; how much less future money is worth than present money.

Let's say this is 4%.

2. Equity Risk Premium

This is what investors demand for taking on the volatility and uncertainty of owning equities versus safer assets like cash. Let's say this is around 5%.

Put together with the risk-free rate, it explains why if you ask people what they expect from long-term equity rates of return, many would say something like 9% (the 4% cost of the time value of money plus the other 5% required to compensate for the general risk of equity). People will give different numbers for this expectation at different times, which makes some sense given different risk-free rates and different perceptions of risk.

3. Industry Risk Premium

Some industries are simply riskier than others. A biotech startup faces different odds than a utility company. Some products and services sell differently depending on the economy, others don't depend much on what changes. You don’t control the inherent volatility of the sector, but you do choose which industry you’re in and which business lines you emphasize. In the sense that you choose what business to be in, you have some control here, but once your business is well underway, you're stuck with the risk you have.

Taken together, these first three components reflect the cost of capital in the world at large, not the details of your business.

Part 2: What You Do Control

Here’s where things get interesting, because these are the levers that directly influence your discount rate, your valuation multiple, and potentially your long-term wealth.

4. Size Premium

Smaller companies are, all else being equal, riskier. Not because they're poorly run, but because they likely lack diversification relative to larger companies.

For example, a business doing $1B in revenue must pretty much by definition:

- serve many customers

- operate across multiple geographies

- have several product lines

- rely on diverse teams and processes

A business doing $50,000 in revenue would very likely rely on:

- a handful of clients

- a single owner/operator

- maybe one main product or service

- a small, local market

The larger company can survive more forms of “hits.” The smaller company can’t.

This is why growth to a larger size itself reduces risk and lowers the discount rate. Don't confuse this with "growth rate." While it's true that a business that demonstrates faster growth will (pretty famously) also likely have a higher valuation, this component is really about the scale at which you operate.

5. Company-Specific Risk Premium

Once we’ve accounted for size, industry, and general market forces, the rest comes down to you, and the specifics of what you have set up in your business ("idiosyncratic risk"):

- Are operations consistent or variable?

- Is too much revenue tied to one or two people (internal or external)?

- Is the business dependent on the owner’s or another employee's personal relationships?

- Are there looming legal, financial, or operational risks?

- Is there customer or supplier over-concentration?

- Is documentation poor or systems nonexistent?

- Is past performance very likely to be predictably replicated and expanded, or is that too hard to predict?

This final piece, company-specific risk, is where two businesses with identical financials can have drastically different valuations. Also, depending on scale, it could be the greatest contributor to your company's discount rate, which in turn means a lower valuation for your company.

So Why Does This Matter?

Because the discount rate measures how risky your future cash flows are.

When you project sales growth, the real question is: How likely is that growth to actually happen?

When you estimate how much revenue converts into cash flow, the question becomes: How reliable are your operations, your people, and your margins?

By breaking down the discount rate, you gain a roadmap for improving value:

You can grow cash flow, which most business owners are already constantly working on…

or you can reduce the discount rate and improve your multiplier.

Cash flow is the lifeblood of a business, but it also increases value linearly.

Core improvements to the reliability of your business (and thus reduce the discount rate) increase value exponentially.

Even If You’re Not Selling, This Analysis Matters

A business with a high discount rate is:

- volatile

- stressful

- harder to operate

- more dependent on the owner

- more vulnerable to bad luck

So yes, discount rates affect value to a buyer. But they also reveal whether your company is healthy and resilient, or fragile and exhausting.

A low-value business is almost always a high-hassle business. A business worth more to others should also be worth more to you.

Finally, if you plan to hold a business for life and benefit from its cash flows for decades into the future, don't you want to be sure that those future cash flows can be relied upon for you and your family?

The Takeaway

Understanding the discount rate, and more importantly, the components you can control, gives you a powerful framework for improving your business.

It helps you:

- prioritize what to fix

- understand what really drives value

- distinguish between revenue growth and quality of revenue and growth

- focus on changes that reduce risk, not just increase sales

In short:

This is how you work smarter, not harder, on building your business.

And whether or not you ever plan to sell, that knowledge has real value.